WTF? NEWS

Published Irregularly Weather or Not We Feel Like ItAny Damned Time We Please

Important Dislaimer: In case any reader doesn't quite get it, this is parody protected under the first amendment of the Constitution of United Statements of America. If you don't like the law then feel free to go try and change it. If you are interested in further information on freedom of the press we suggest you start with John Milton's masterful essay "Areopagitica" (1644) http://www.uoregon.edu/~rbear/areopagitica.html

Biden: "Even If We Do Everything Absolutely Right We Have a 30% Chance of Stimulus Failing"

With Statements Like That Who Needs Skeptics?

Confidential Memo

To: Joe Biden, VPOTUS

From: Agent Stickman, Obama Admistration Double Secret Financial Operative

Re: "Only 70% Probability of Stimulus Working"

I have surrepticiously received numerous emails from around the globe expressing concern at best to downright consternation regarding your comments as reported in the Wall Street Journal that the $900 billion fiscal stimulus has only a 70% chance of success. As your personal communications coach, I suggest using, for messaging purposes, a little less candor regarding the "Hail Mary" attributes of the "4th down and 36 yard" stimulus package. I mean come on! If this thing has a 30% probability of failing if we get it exactly right (which we know we won't) don't you think some people might say, "if can't we come up with something a little more thoughtful w/t/f are we doing this for?" I might, as add food for thought Mr. Vice President that lemmings who change their minds in mid-air following their comrades over the cliff have a very short window of mental clarity.

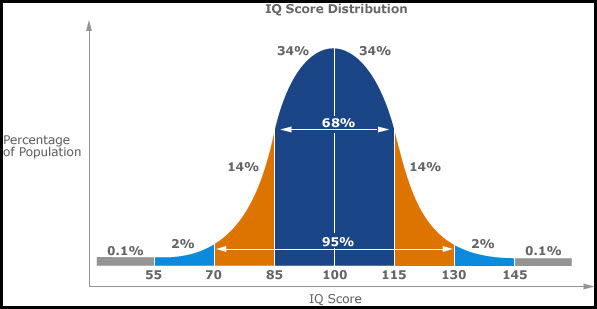

While I don't necessarily disagree with your probability assessment (personally, I handicap this puppy of a stimulus as 50-50 proposition a best) but I would never admit that publicly particularly when President Obama is trying to re-assure people that this thing is going to work. Perhaps if you could revise your word framing and estimate of success to fall more comfortably within 1 standard deviation of the expected mean outcome (see below) it would really help the market avoid the uderstandable impression we have absolutely no idea what we are doing other than what we are doing is gonna be really big. I do hope I haven't overstepped my bounds but that's what you're paying me for sir. My best advice, with all due respect Mr. Vice President might just be to shut the f*** up. People will start to confuse you with former Secretary Paulson. I wll carry at all times an updated resume (for you and me) so if this sick puppy turns out to be a dead dog Iwe are prepared for the 2010 mid-terms.

Caveat Emperor

Stickman

From Wall Street Journal

February 6, 2009, 11:27 am

Biden Urges Passage of Stimulus Despite Voter Backlash

Susan Davis reports from Williamsburg, Va., on the House Democrats’ retreat.

Vice President Joe Biden acknowledged today that Democrats could face political repercussions in 2010 fortheir support of the $900 billion economic stimulus package. “But when we do [approve it], I’m sure you’re going to be nailed in ads, ‘Well they voted on that’ 30 second ads,” Biden told roughly 200 members of the House Democratic Caucus gathered here for their three day annual retreat. “I promise you as [a colleague] once said to me, ‘I’ll come campaign for you or against you, whichever will help you the most in your district.’ And so will the president because, again, we’re all in this together.”

Vice President Joe Biden speaks about the benefits of the economic stimulus bill at a local train station in Laurel, Md., Thursday.

Vice President Joe Biden speaks about the benefits of the economic stimulus bill at a local train station in Laurel, Md., Thursday.

Cultural Icon Alfred E. Newman expressed grave concern about the stimulus package

Cultural Icon Alfred E. Newman expressed grave concern about the stimulus package

The vice president also offered some trademark candor about the prospects of success.

He recalled a recent White House meeting with the president and senior aides in which they were discussing the many challenges the country faces. “If we do everything right, if we do it with absolute certainty, there’s still a 30% chance we’re going to get it wrong,” was his message at the meeting.

Biden warned that the consequences were too great for the country to allow politics to prevent action. “The only thing we can get wrong is not reaching a consensus among ourselves…and demonstrating to the American people that we’re thinking small and politically—you [House Democrats] have not, you’ve thought big,” he said. All but 10 House Democrats voted for the bill.

Echoing President Barack Obama’s remarks here Thursday, Biden aligned this moment with other great challenges the country has faced. “Not since World War II has a caucus gathered with so many challenges facing our country and the stakes so high,” he said. “The slope is pretty steep. The opportunities are great.”

Biden noted that history suggests many of the smart decisions made to aid the nation were unpopular, and that Congress will have to take tough votes. “There were very few decisions that were made [back then] that were popular,” he said. “That’s the bad news folks.”

Yet Biden sought to strike an optimistic tone here and underscored the importance of unity in the ranks. “This is about all of us, we’re in this together,” he said, and “when it works, as I’m absolutely convinced it will, I’m absolutely convinced, that our best days are ahead of us. I’m not just saying that, I really believe that with every fiber in my being that this is an opportunity.”

Perhaps it wasn't clear to Secretary of Treasury Geitner from lame-duck George Bush's overture last December to the G Whatever when he sent out a very thoughtful and well prepared invitation: "hey guys why don't you pop over to the White House for beer while you're all in town and see if we can stabilize the financial markets and then have a group photo opp we can put out on the wire so it looks like we are all working together?" BIG success. Worked like a charm. So off to Rome goes Geitner to sell, sell, sell.

Perhaps it wasn't clear to Secretary of Treasury Geitner from lame-duck George Bush's overture last December to the G Whatever when he sent out a very thoughtful and well prepared invitation: "hey guys why don't you pop over to the White House for beer while you're all in town and see if we can stabilize the financial markets and then have a group photo opp we can put out on the wire so it looks like we are all working together?" BIG success. Worked like a charm. So off to Rome goes Geitner to sell, sell, sell. Post a Comment

Post a Comment